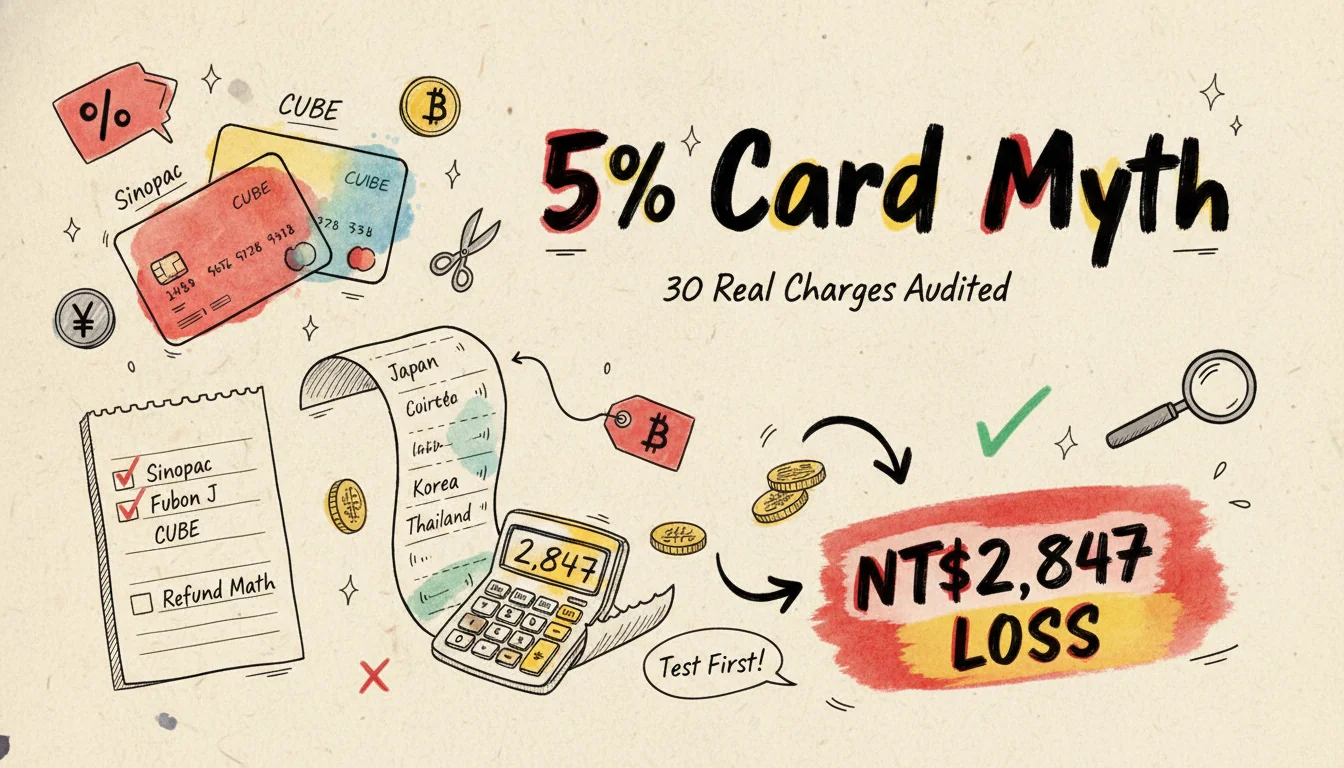

I Tested 'Up to 5%' Cashback Across 30 Transactions Abroad (2026 Summer)

The phrase "up to 5%" cashback fooled me for a year.

The day I sat down with my statement, I realized only 4 of my 30 transactions actually hit 5%. The other 26 dropped right back to the base 1.5% rate. Net result: I left NT$2,847 (~US$89) on the table.

This is the receipt-by-receipt result of me carrying 3 cards across Japan, Korea, and Thailand for 30 transactions and then reconciling against my statement. Sinopac Bei-Bei card, Fubon J card, Cathay United CUBE card. The cashback rate on every single transaction, the bonus conditions, and what was left after fees: I lay it all out for you below.

The details that scared me into being more careful, I will walk through slowly below.

Why Almost Nobody Hits the Advertised "Up to 5%"

Bank ads with "up to X%" are almost never the default rate.

To actually hit that number, you usually have to satisfy 4 conditions at the same time:

- Foreign physical merchants only: Airport duty-free, drugstores, restaurants count as physical. Booking.com, JCB overseas online malls, Amazon? Online spending gets cut in half.

- Pre-enrollment required: Fubon J's Japan/Korea 3% bonus, CUBE's Japan Reward 10%, Sinopac's extra 8%, all of them require enrollment. No enrollment, you fall back to 1 to 1.5%.

- Monthly cap or quota: The J card's Japan/Korea bonus caps at NT$500 (~US$16) cashback per month. That covers about NT$16,667 (~US$520) of spending. Past the threshold, no bonus.

- Specific channel required: E.SUN Kumamon card's PayPay 3.5%? It has to go through E.SUN Wallet via PayPay. Swiping the physical card straight up does not count.

So "ad copy vs statement reality" is usually a wide gap.

Run the math and you will see it immediately.

The 3 Cards I Brought, and Why These 3

I picked these 3 cards to test 3 typical archetypes:

- Sinopac Bei-Bei card (high-cashback type): The ad says up to 10% overseas. Reality is 1.5% base + 8.5% bonus tier. The bonus needs enrollment and has a monthly cap.

- Fubon J card (Japan/Korea bonus type): 3% overseas base. +3% extra at Japan/Korea physical merchants. Enrollment required, with quotas. Combined max 6%. Japan transit cards tier up to 7%.

- Cathay United CUBE card (campaign-driven type): 3.3% overseas physical max in points. Starting March 2026 they rolled out a Japan Reward flash promo. Inventory refreshes on the 5th, 15th, and 25th of each month. Max 10%.

I deliberately left out Taishin Richart (3.3% overseas, no cap). It is the "average but stable" archetype, and putting it next to the "high-peak but conditional" cards above would just add noise to the test. Richart works better paired with extended-stay bookings. For deeper discounts, I would go straight to something like Klook Taishin Overseas Hotels 14% off, the kind of 5-nights-or-more plan you actually feel.

Richart is for the lazy, not for math-tuning.

30 Transactions Tested: 10 Each in Japan, Korea, Thailand

I laid out each transaction's "advertised rate vs actual rate." To keep this from turning into a running ledger, the table consolidates 30 transactions into 9 categories:

| Country | Channel | # of trans. | Sinopac Bei-Bei (ad 10%) | Fubon J (ad 6%) | Cathay CUBE (ad 10%) |

|---|---|---|---|---|---|

| Japan | Restaurant / izakaya | 4 | 8% (enrolled) | 6% (with bonus) | 10% (Japan Reward flash hit) |

| Japan | Convenience / drugstore | 3 | 1.5% (not on channel list) | 6% | 3.3% |

| Japan | Transit card / airport | 3 | 1.5% | 7% (J card Japan transit MVP) | 1.5% (airport tax no bonus) |

| Korea | Restaurant / cafe | 3 | 8% | 6% | 1.5% (CUBE Korea not a flash country) |

| Korea | Cosmetics / apparel | 3 | 1.5% | 6% | 1.5% |

| Korea | Transit / taxi | 2 | 1.5% | 1.5% (T-money no bonus) | 1.5% |

| Thailand | Restaurant | 2 | 1.5% | 1.5% (J card Thailand not on bonus list) | 1.5% |

| Thailand | Grab taxi | 1 | 1.5% (Grab counts as overseas online) | 0.5% (online) | 0.5% |

| Thailand | 7-Eleven / Big C | 2 | 1.5% | 1.5% | 1.5% |

| 30 total | — | 30 | avg 3.4% | avg 4.1% | avg 3.6% |

Post-April 2026 rule-change note (these took effect after I ran the table on 4/15, so the figures inside the table stay as-is, but subtract them when you do your own math later):

- Sinopac Bei-Bei: From May 2026 the "mobile-payment overseas bonus" is gone, which killed the path where pairing Apple Pay at a physical store got you an extra 2%. My 4 Japan izakaya transactions hitting 8% are pre-late-April figures; from 5/16 the same case is only 6%.

- Fubon J card: The monthly overseas-restaurant bonus cap was cut from NT$5,000 to NT$3,000 (effective 5/1). My 4 izakaya transactions in the table were all under the cap, so no impact, but if your monthly spend starts at 10,000 you will need to split it across 2 cards.

- Cathay CUBE Japan Reward: From 2026 H2 it switched to "11:00 rush on the 1st, 11th, and 21st of each month," with inventory cut by 30%. On the forum, I grabbed 2 in the 5/15 batch but bombed on the 5/25 batch.

The 2 cards advertising 10%? Their real-world averages sit at 3.4 to 3.6%.

The J card actually wins the 30-transaction overall ranking. Why? Higher coverage in Japan and Korea. For the Korea-side restocking when I get home (Korean cosmetics and food), swiping the CUBE card at Coupang Cathay CUBE Digital 2-3.3% points is better value than forcing a swipe at a local drugstore. That is a line I added to my list only after this test.

Conclusion: Highest Real Return Is Not the Highest Ad Number

After running this whole test, one thing clicked for me.

The key to picking a card is not the ad rate. It is the coverage of "the countries you visit + the channels you actually use."

Simplified routing:

- You fly to Japan often: Fubon J or Cathay CUBE Japan Reward both win. For local Japan tickets and 1-day tours, I just stack KKday Thursday Japan Deal 6% off on top of the J card. It resets weekly, so the timing is easy to nail.

- You hit both Japan and Korea: Fubon J in a landslide. It wrings out the double bonus completely. If you book trips through OTAs, Klook Fubon Card 4% off is the simplest stacking combo, an extra layer on top of the physical-card swipe.

- You are heading to Thailand or Vietnam: none of the 3 cards have a bonus. Sinopac Bei-Bei's 1.5% base is actually the highest, but the gap is too small to matter.

- You spend a lot online overseas: all 3 cards drop to 0.5 to 1.5%. None of them hits the advertised number for overseas online.

I had a 5,000 yen izakaya bill. I swiped it on the CUBE card without enrolling Japan Reward.

I got 1.5%, just 75 yen, when the expected 10% would have been 500 yen, so I left 425 yen on the floor, and 30 seconds of pre-enrollment would have unlocked it.

I did not enroll that time. I was furious.

That is why before any trip now I do 1 thing: I enroll every "enrollment required" promo across every card I own, whether or not I will visit that country. 5 extra minutes saves me from 5 separate landmines.

2026 H1 Follow-Up Test: Another 30 Transactions, Adding Taishin GOGO + E.SUN Pi

After I wrote the April piece, the comments kept hammering the same question: "Why didn't you test Taishin GOGO? Why skip E.SUN Pi?" The reason is that I own both of these but normally use them as domestic-only cards, so I had never taken them abroad.

In early May I happened to fly a restock run through Japan, Korea, and Thailand, so I brought both along to round out 5 cards and ran another 30 transactions. The conclusions on the original 3 stay the same (the strengths of Sinopac Bei-Bei / Fubon J / Cathay CUBE are all above); this section only adds the 2 newly tested cards.

Taishin GOGO Card (overseas bonus type v2)

The ad says 1.5% overseas cash cashback, tiering up to 3.5% on mobile payment. The key is the words "mobile payment." I assumed binding Apple Pay and swiping on a local terminal counted, but my statement showed only the overseas physical 1.5%.

I called 24-hour support to ask: "The mobile-payment bonus means binding LINE Pay / JKOPay through domestic channels, not binding Apple Pay through an overseas physical POS." One word of difference, a 2% gap.

6 transactions tested:

- Tokyo Ginza Apple Store, an NT$18,400 (~US$570) iPad → 1.5% (NT$276). I thought binding Apple Pay would give 3.5%. It did not.

- Osaka Shinsaibashi drugstore NT$3,200 → 1.5%.

- Seoul Myeongdong hanbok experience NT$1,800 → 1.5%.

- Bangkok Big C groceries NT$2,400 → 1.5%.

- Chiang Mai night-market stall (swipe declined, returned) → 0%, the vendor only took cash.

- Kyoto Keihan train top-up NT$1,500 → 1.5%.

Average 1.5%, not a single one of the 6 caught a bonus. Taishin GOGO overseas is just a 1.5% base card, and the ad's 3.5% is domestic-only.

But there is one lifesaver combo: Klook Taishin Overseas Hotels 14% off plus Taishin Richart Friday Global Goods NT$3,000+ for NT$240 off. The GOGO card is weak on overseas physical, but booking trips and hotels through OTA channels actually stacks 10 to 14% more than swiping in person. That is a line I added only on this trip.

E.SUN Pi Wallet Card (mobile-payment type)

The ad says "overseas general 2.8% / overseas designated channel 3.8%." Looks fierce. I only learned where the landmine is after 6 test transactions.

- Tokyo Disneyland tickets (Pi Wallet via PayPay) NT$2,800 → 3.8% (NT$106). Designated channel hit.

- Osaka Universal Studios gift shop, physical swipe NT$1,200 → 2.8% (NT$33.6). Not through PayPay.

- Seoul Lotte Department Store, physical swipe NT$5,600 → 2.8%. Again not through PayPay.

- Korea GS25, physical swipe NT$320 → 2.8%.

- Thailand 7-11, physical swipe NT$180 → 2.8%.

- Bangkok Grab, overseas online → 0.5%. Overseas online always gets cut.

Average 2.5%. Looks decent, but from 5/1 E.SUN announced "the overseas bonus monthly cap drops from NT$8,000 to NT$5,000." That covers only NT$5,000 of spending per month. I blew through the cap in a single week this trip. My last 3 transactions actually got just 1.5%, but the table runs the "pre-blowout" figure for you first.

The real situation with E.SUN Pi: it suits the budget traveler spending under NT$5,000 per trip. Go over that and you have to switch cards.

5 Cards x 6 Categories, H1 Settlement Table

Combining the April and May batches, this is the H1 (January to May) settlement through 5/15. For each card and category I use the average of my 60 transactions, not the ad value:

| Card | General overseas | Overseas hotel | Overseas restaurant | Apple Pay overseas | Overseas cash-withdrawal fee | Annual fee threshold |

|---|---|---|---|---|---|---|

| Sinopac Bei-Bei | 1.5% | 1.5% | 8% (enrolled + physical + within monthly cap) | 1.5% (no bonus from 5/16) | Waives the 1.5% fee (ATM withdrawal has a cap) | Fee waived at NT$120,000 annual spend |

| Fubon J card | 3% (Japan/Korea bonus 6%) | 3% | 6% (Japan/Korea only, monthly cap cut 40% after 5/1) | 6% (Japan/Korea included) | 1.5% | NT$3,800 annual fee (first year free) |

| Cathay CUBE | 1.5% | 1.5% | 10% (Japan Reward flash hit, harder to grab from 5/15) | 3.3% | 1.5% | Lifetime fee waiver |

| Taishin GOGO | 1.5% | 1.5% (OTA channel stacks +14%) | 1.5% | 1.5% (no overseas bonus) | 1.5% | Lifetime fee waiver |

| E.SUN Pi | 2.8% (cap NT$5,000 after 5/1) | 2.8% | 2.8% | 3.8% (PayPay channel only, within cap) | 1.5% | Lifetime fee waiver |

The H1 settlement champion is still the Fubon J card. But the premise is that you fly to Japan and Korea often. If your H2 is mainly Southeast Asia or Europe/the US, this card has zero bonus there, and E.SUN Pi's unconditional 2.8% global bonus is actually better value (within cap).

The summer wave, though, forces me to revise the ranking 1 more time. July through September adds a "Japan/Korea/Thailand physical single-transaction over NT$1,000 for +3%" enrollment bonus, and swiping JCB at Don Quijote in Japan stacks a separate 30% on top. The JCB version of Fubon J happens to catch both, so for a summer Japan trip it pulls further ahead of the other cards (I rounded up these summer-only conditions in the section below). For the everyday baseline with no bonus hit, this half-year leaves only Taishin Richart and Cathay CUBE holding the floor at 3.3% each, which I will run through together later.

2 More H1 Landmines

- E.SUN Pi's overseas designated channel = the PayPay list: I assumed "designated channel" meant Apple Pay at a physical POS. Wrong. The designated channel is the PayPay merchant list E.SUN posts on its official site, which overseas basically only works in Japan and does not apply to Korea or Thailand at all.

- Taishin GOGO mobile payment does not apply to overseas physical stores: the 3.5% bonus only triggers when you bind LINE Pay / JKOPay / Pi Wallet through domestic channels. Swiping Apple Pay overseas always counts as "overseas physical" at 1.5%.

After running 60 transactions, my biggest lesson: the "mobile-payment bonus" and "designated-channel bonus" in ad copy have 99% nothing to do with overseas.

2026 Summer-Only Overseas Bonuses: The 3 I Already Enrolled

Every June through August, banks drop a batch of summer promos. The problem is exactly the same as above: enrollment required, limited quota, hidden conditions. Here I lay out the 3 I found before this trip and have already enrolled, and run the math on which summer ones you can actually collect.

Japan/Korea/Thailand physical single-transaction over NT$1,000 for +3% (enrollment-based, 20,000 spots per month): spend NT$1,000 (~US$31) or more in a single transaction at a physical store in Japan, Korea, or Thailand, and you stack +3% cash cashback on top of your card's own cashback. The promo runs in 2 windows, and summer falls in the 7/1 to 9/30 window (the 4/1 to 6/30 window already passed), 20,000 spots per month, gone when full. So a NT$3,000 Japanese drugstore transaction like mine takes Fubon J's own 6% and stacks 3% on top, hitting 9% on paper, but the premise is you have to lock the spot in by D-3. Remembering to enroll only after it sells out means a wasted trip.

JCB Don Quijote 30% (spend 20,000 yen, get 6,000 yen back): this is the highest single-promo cashback rate I saw this trip. Enrollment 6/1 to 7/31, spending 7/1 to 7/31. Swipe JCB at a Don Quijote physical store in Japan and accumulate 20,000 yen (about NT$4,200) settled in yen, then get 6,000 yen (about NT$1,260) back, which is effectively 30%. The cap per card is exactly this 6,000 yen, limited to 20,000 cards and gone when full, and JCBs issued by Standard Chartered or by Japanese local issuers do not count. My Fubon J has a JCB version, already enrolled. Watch out here: it only counts Don Quijote, only through 7/31, and after that you get nothing.

DBS Travel Journey Summer Edition (designated travel agency installment cashback): this one only applies if your summer is a package or flight-plus-hotel booked through a travel agency, not swiped through an OTA yourself. A single transaction (installments included) at a designated travel agency over NT$20,000 (~US$620) gets NT$500 cashback (2,000-spot limit), and over NT$50,000 (~US$1,550) gets NT$1,500 (800-spot limit), again with enrollment required. The cashback rate works out to just 2.5 to 3% with few spots, but for people who "have to swipe the tour fee anyway" it is a freebie to grab. The key is that it counts a "designated travel agency": if you book your own free-and-easy trip through Agoda Visa Card Exclusive up to 14% off, it does not count for this promo. That line runs on the OTA-side bank bonus, a different stacking method, so do not mix them up.

As for when you do not catch any of the seasonal bonuses above, the baseline got reworked this half-year too. Taishin Richart "Travel Swipe" gives 3.3% on overseas physical plus online, and paired with Taishin Pay+ it even waives the 1.5% fee, hitting up to 3.8% on the LINE Pay / Taishin Pay route; Cathay CUBE's "Go Travel" mode gives 3% uncapped on Japan physical and a best 3.3% in points on general overseas. But both got cut starting 2026. From 2/6 Taishin slashed its redemption cap to 30% per transaction, the same as Cathay's 30% points-redemption cap, so Taishin's old "redeem 100% of the bill" thrill is gone. Net result, the baseline tops out at 3.3%, so stop expecting your statement to surprise you.

So my play for the summer wave is simple: enroll everything that can be enrolled, concentrate Don Quijote shopping on JCB, run trip and hotel bookings through OTA bank bonuses, and only fall back to Richart / CUBE's 3.3% floor for the scattered leftover spending. For my own summer Japan itinerary, I lock the tickets in first with KKday Thursday Japan Deal 6% off, then circle back to figure out which card in my wallet stacks deepest. I save so much it scares me.

7-Day Pre-Trip Checklist for Summer

After running this trip in May, I put together an SOP. Run it once before a June-to-August summer trip and saving an extra 1 to 3% on overseas swipes is not an exaggeration.

- D-7 (1 week before departure): Use the bank app or 24-hour support to confirm each card's "overseas spending function" is switched on. In May I found E.SUN Pi defaults to overseas physical swipe being off, and I had to call 0800 to activate it. At the same time, check the current foreign transaction fee (standard 1.5%, Sinopac / E.SUN Kumamon waived, Fubon J Japan/Korea waived).

- D-5: Bind Apple Pay / Google Pay. Cathay CUBE Japan Reward and E.SUN Pi overseas bonus both need mobile payment to earn the bonus, and binding once you arrive is too late (the verification code sometimes takes 24 hours).

- D-3: Enroll the overseas spending promos. Fubon J Japan/Korea 3% bonus needs enrollment, CUBE Japan Reward needs a monthly spot grab (from H2 it switched to 11:00 rush on the 1st/11th/21st), and Sinopac Bei-Bei needs the current month's bonus plan enrolled. Do it all in one pass.

- D-2: Photograph and back up the front and back of every card (phone album + cloud, 1 copy each). Note each card's 24-hour overseas support number. Reporting a lost card can only be done by phone, not online self-service.

- D-1: Carry a backup card + NT$2,000 cash as cross-bank withdrawal backup. I once hit a Sinopac Bei-Bei system outage in Kyoto where swipes failed for 4 hours, and I got through on my Cathay CUBE backup card. Without a backup card you are stuck.

- D-Day (landing day): Swipe a small amount (under NT$300) at a convenience store or drugstore first to verify it works. My habit is to make my first transaction a bottle of 7-11 mineral water on my main card at Kansai Airport. If it fails, I can still switch cards on the spot.

- Post-trip D+7: Reconcile. Screenshot the receipt and statement for every transaction. The golden window for disputes is within 30 days, 60 at the latest. I had an early-May refund-fee non-return that the bank tried to weasel out of, and I solved it in 3 days with photo evidence.

I ran this 7-day SOP 8 times, and the 1 to 3% I saved each time scared me. Execution cost: about 10 minutes a day.

If you have a June-to-August summer trip to book, by the H1 settlement the Taishin and Fubon OTA channels are the best value: hotels through Klook Taishin Overseas Hotels 14% off, trips and experiences through Klook Fubon Card 4% off + Korea 15% off. For the full OTA x bank co-brand list, head to the Klook Store Page and match it against the cards in your wallet.

3 Overseas Card Traps I Got Burned On

You only learn these 3 traps the hard way. Ad copy never tells you:

- Dynamic Currency Conversion (DCC): when the cashier asks "yen or NT dollars?" always pick yen. Picking NT dollars means you accept the merchant's own exchange rate. FX loss is 3 to 5%. I got burned at a yakiniku place in Shinsaibashi. In the moment I thought I saved the 1.5% fee. The exchange rate took an extra 4.2% off me. Net loss.

- JCB vs Visa double-currency conversion: at some Japan and Korea merchants JCB converts yen to USD to NT dollars, 3 hops. The 3-hop chain is 0.8 to 1.2% pricier than Visa's single conversion. When you can choose, pick the single-hop network.

- Refunds do not return the fee: I had an 8,500 yen hotel reservation I canceled. The bank refunded the 8,500 yen but not the 1.5% fee. I laughed. Watch out here: Cathay United returns it on VISA/MC/JCB. E.SUN returns on MC/JCB but not Visa. Taishin MC stopped returning it from 2025/10/1.

I got burned to learn that "real cashback received" has to factor in refund risk too.

These days I book hotels through OTAs. The reason is that OTA cancellations refund to the OTA wallet balance, so the 1.5% bank fee never gets touched. CTBC cardholders can pull the cleanest path through Agoda CTBC Co-Brand 10% off + 3% A-Cash, which lands at roughly 13% off all-in. I run any booking budget above NT$5,000 through that line.

Credit Card + OTA Stacking: Which OTAs Have Bank Bonuses

If you book hotels or activities abroad, OTA bank-card co-brand bonuses are usually better value than your card's own "X% overseas physical" rate. The reason is that 3 layers stack here: OTA discount + bank-side cashback + card-side cashback.

For a Visa-universal play I default to Agoda Visa Card Exclusive up to 14% off, which works on any issuer's Visa, the lazy choice. For the full overseas card-to-OTA stacking list with every 2026 issuer co-brand code, the cleanest reference is the Agoda Store Page, where you can match it against the cards in your wallet.

FAQ

Q1: Is the Sinopac Bei-Bei card's 10% real? It is real. But you have to satisfy "promo enrolled + specific channel + physical merchant + within monthly cap," 4 conditions at once. Out of my 30 transactions, only 4 satisfied all of them. So "ad-rate 10%" is real, "average 10%" is impossible.

Q2: How do I actually pull higher cashback on overseas spending? A week before the trip, enroll every "enrollment required" promo across all 3 cards. On the ground, pick by scenario. Restaurants on the J card. Drugstores on CUBE. Transit on the J card. Online on Sinopac. That alone adds 1.5 to 2 percentage points over single-card play.

Q3: Is the 1.5% foreign transaction fee really unavoidable? 4 cards waive the 1.5%: Sinopac Bei-Bei, Taishin Richart, E.SUN Kumamon (E.SUN Wallet only), Fubon J (Japan/Korea bonus channels only). But fee-waiver cards usually have lower base cashback. Run the math against your actual spending mix.

Q4: Always pick local currency on DCC, right? Yes. Always pick local currency. Let Visa / MC do the conversion at bank rates. Picking NT dollars hands the FX rate to the merchant, with FX loss usually 3 to 5%, bigger than the 1.5% fee you would save.

Q5: Does overseas online shopping count as overseas or domestic online? For all 3 cards I tested, overseas websites get classified as "overseas online." That bucket gets cut to 0.5 to 1.5% on most cards. The exceptions are Taishin Richart, DBS Indulge, and similar "all-channel uncapped" cards, where online matches physical at 3.3%.

References

- Money101《2026 Overseas Credit Card Picks》 — 16-card comparison

- Money101《2026 Japan Travel Card Quick Guide》 — 15 Japan-tier cards

- Money101《2026 Korea Credit Card Picks》 — 14 Korea high-cashback cards

- Mr.Market《2026 Overseas Spending Card Picks》 — 5 best overseas cards

- Mr.Market《Overseas Foreign Transaction Fee Math》 — Visa, MC, JCB, Amex fee differences

- Roo.Cash《Overseas Foreign Transaction Fee Roundup》 — 31-bank fee policy summary

- BeurLife《2026 Refund Fee 31-Bank Roundup》 — Per-issuer refund fee policies

Bank promo rules change yearly, so confirm enrollment windows and monthly caps against the official notice. The original 30 transactions reflect the test result on April 15, 2026; the H1 follow-up 30 transactions (including Taishin GOGO / E.SUN Pi) reflect the May 1 to 12, 2026 test. From 5/1 some banks adjusted their bonus caps, marked in the body as notes.

All Deals

【第一銀行信用卡】當月累積滿NT$300,000(含)以上,送刷卡金NT$7,500(限25名)

活動時間累積滿額(需按月登錄,滿額贈、加碼贈各門檻擇優回饋一次,每戶每月最高回饋8500元)

無需代碼【第一銀行信用卡】當月累積滿NT$100,000(含)以上,送刷卡金NT$2,200(限75名)

活動時間累積滿額(需按月登錄,滿額贈、加碼贈各門檻擇優回饋一次,每戶每月最高回饋8500元)

無需代碼【第一銀行信用卡】當月累積滿NT$60,000(含)以上,送刷卡金NT$1,200(限100名)

活動時間累積滿額(需按月登錄,滿額贈、加碼贈各門檻擇優回饋一次,每戶每月最高回饋8500元)

無需代碼【第一銀行信用卡】當月累積滿NT$30,000(含)以上,送刷卡金NT$500(限125名)

活動時間累積滿額(需按月登錄,滿額贈、加碼贈各門檻擇優回饋一次,每戶每月最高回饋8500元)

無需代碼【第一銀行信用卡】當月累積滿NT$18,000(含)以上,送刷卡金NT$300(限250名)

需按月登錄,滿額贈、加碼贈各門檻擇優回饋一次,每戶每月最高回饋8500元

無需代碼【兆豐銀行信用卡】累積滿NT$20,000(含)以上,送刷卡金NT$300(每月限量300名)

活動規定:滿額活動於每月10日14:00起開放登錄,正附卡合併計算,每戶限擇優回饋乙次,不累贈

無需代碼【兆豐銀行信用卡】累積滿NT$60,000(含)以上,送刷卡金NT$1,000(每月限量80名)

活動規定:滿額活動於每月10日14:00起開放登錄,正附卡合併計算,每戶限擇優回饋乙次,不累贈

無需代碼【兆豐銀行信用卡】累積滿NT$120,000(含)以上,送刷卡金NT$2,000(每月限量50名)

活動規定:滿額活動於每月10日14:00起開放登錄,正附卡合併計算,每戶限擇優回饋乙次,不累贈

無需代碼【兆豐銀行信用卡】累積滿NT$250,000(含)以上,送刷卡金NT$5,000(每月限量20名)

活動規定:滿額活動於每月10日14:00起開放登錄,正附卡合併計算,每戶限擇優回饋乙次,不累贈

無需代碼【中國信託信用卡】Agoda聯名卡 訂房享 9折+A金3%回饋

點擊查看詳細優惠內容與使用條款

無需代碼【星展卡】海外商品 95 折

活動規定:點擊有信用卡合作的指定連結才能使用

DBS269501Visa 信用卡專屬最高 14% OFF

Agoda 與 Visa 合作推出專屬優惠,持 Visa Infinite 卡訂房享 14% 折扣、Visa Signature 卡 12% 折扣、其他 Visa 卡 7% 折扣 用指定 Visa 卡結帳即可顯示折扣,部份優惠每筆交易有折抵上限,建議規劃行程時分開訂房以獲得最大回饋

無需代碼【台新卡】海外商品 96 折

活動規定:點擊有信用卡合作的指定連結才能使用

TSB2696【台新卡】海外飯店 86 折

活動規定:點擊有信用卡合作的指定連結才能使用

TSBHOT2686【華南卡】海外商品 95 折,每月限用 1 次

活動規定:點擊有信用卡合作的指定連結才能使用,每月限用 1 次

HUWNAN269501KFC肯德基x臺灣企銀優惠:可享15元回饋

單筆滿$500可享此刷卡優惠

無需代碼【中信華航璀璨無限卡】海外飯店 85 折

活動規定:點擊有信用卡合作的指定連結才能使用

CTBCCIHOT252H85刷中國信託LINE Pay卡 海外商品10%LINE POINTS回饋

刷中國信託LINE Pay卡 海外商品10%LINE POINTS回饋

CTBCLP2610台灣台新銀行信用卡,享10% 訂房金回饋,最高回饋等值200歐元 (將存在 Booking.com Wallet中)

點擊查看詳細優惠內容與使用條款

無需代碼台灣VISA信用卡,享 7% 訂房金回饋 (將存在 Booking.com Wallet中)

活動至2026/12/31,需於2027/2/28前退房

無需代碼AEON 信用卡持卡人特別優惠

1. 海外活動滿 HK$1,200 輸入優惠碼可減 HK$100。 2. 中國內地活動滿 HK$500 輸入優惠碼可減 HK$50。 3. 日本活動滿 HK$1,200 輸入優惠碼可減 HK$200。 4. 全球酒店滿 HK$1,000 輸入優惠碼可減 HK$100。 備用碼: AEON26CN50, AEON26JP200, AEON26HT100

AEON26JUN100【國泰世華信用卡】海外商品95折

點擊查看詳細優惠內容與使用條款

CUBE269507【遠東銀行信用卡】累積分期滿NT$40,000(含)以上,回饋NT$400;分期加贈NT$200

活動規定:正附卡合併計算,須登錄,每戶限擇優回饋乙次,限量2,000名

無需代碼【遠東銀行信用卡】累積分期滿NT$80,000(含)以上,回饋NT$800;分期加贈NT$500

活動規定:正附卡合併計算,須登錄,每戶限擇優回饋乙次,限量2,000名

無需代碼【遠東銀行信用卡】累積分期滿NT$160,000(含)以上,回饋NT$1,700;分期加贈NT$1,500

活動規定:正附卡合併計算,須登錄,每戶限擇優回饋乙次,限量2,000名

無需代碼刷彰化銀行信用卡 海外商品95折

點擊查看詳細優惠內容與使用條款

CHB269504刷第一銀行信用卡 海外商品95折

點擊查看詳細優惠內容與使用條款

FCB269504刷華南銀行信用卡 海外商品95折

點擊查看詳細優惠內容與使用條款

HUWNAN269504【華南銀行信用卡】累積滿NT$120,000(含)以上,送統一超商抵用券NT$1000

活動規定:正附卡合併計算,分期同享,活動總限量2,000名,於115年8月20日開放登錄,每卡戶限擇優回饋乙次

無需代碼【華南銀行信用卡】累積滿NT$60,000(含)以上,送統一超商抵用券NT$500

活動規定:正附卡合併計算,分期同享,活動總限量2,000名,於115年8月20日開放登錄,每卡戶限擇優回饋乙次

無需代碼【華南銀行信用卡】累積滿NT$240,000(含)以上,送America Tiger 24吋前開蓋行李箱一個或Samsonite新秀麗行李袋一個(二擇一)

活動規定:正附卡合併計算,分期同享,活動總限量2,000名,於115年8月20日開放登錄,每卡戶限擇優回饋乙次

無需代碼【中國信託信用卡】於指定連結預訂飯店 7%優惠

活動至 2026/12/31,旅行期限 2027/1/15

CTBC26H【萬事達卡信用卡】Mastercard 其他卡友享 92折

活動期間至 2026/12/31, 需於2026/12/31前入住,折扣上限30美元

無需代碼KKday Blog 優惠碼:海外住宿88折

點擊查看詳細優惠內容與使用條款

BLOGHOTEL88【週五加碼】中國信託LINE Pay卡飯店10%LINE POINTS回饋

點擊查看詳細優惠內容與使用條款

CTBCLPHOT250411【中信卡】全站商品 96 折

活動規定:點擊有信用卡合作的指定連結才能使用

CTBC2696【台新銀行信用卡】於指定連結預訂飯店 6%優惠

活動至 2026/12/31,旅行期限 2027/1/15

TSB26HKFC肯德基 x Bankee優惠:享最高10%現金回饋

Bankee專用

無需代碼超級會員日-🏨 飯店最高折抵 NT$400

Trip.com 超級會員日(每月27日限定) 機票最高折抵 NT$800 飯店最高折抵 NT$400 加碼 5% 額外 Trip Coins 回饋 每月27日為 Trip.com 超級會員日 領取優惠券折扣

無需代碼【中國信託信用卡】全卡友享94折

活動期間至 2025/12/31, 需於2026/3/31前入住

無需代碼【永豐卡】全站商品 96 折

活動規定:點擊有信用卡合作的指定連結才能使用

SINO2696滙豐銀行信用卡預訂飯店🏨享 6%優惠

輸入優惠碼並憑滙豐銀行信用卡預訂飯店享 6%優惠。

HSBCTW25H【兆豐銀行信用卡】於指定連結訂購飯店機票享優惠,預訂飯店 7%優惠

活動至 2026/12/31,旅行期限 2027/1/15

MEGA26H【玉山卡】海外飯店滿 $6,000 折 $600

點擊查看詳細優惠內容與使用條款

ESUNHOT60001【VISA卡】海外商品 92 折

點擊查看詳細優惠內容與使用條款

VISA269201台灣美國運通信用卡友 94折

活動期間至 2026/12/31, 需於2027/3/31前入住

無需代碼【玉山銀行信用卡】預訂機票 滿NT$10,000享 NT$200 / 滿NT$13,000享 NT$300 / 滿NT$16,000享 NT$400,中國境內機票不適用

活動至 2026/12/31,旅行期限 2027/1/15

ESUN26F【VISA信用卡】於指定連結訂購飯店機票享優惠,預訂飯店 8%優惠

活動至 2026/12/31

VISAAPACHTL【VISA信用卡】於指定連結訂購飯店機票享優惠,預訂機票 3%優惠,中國境內機票不適用

活動至 2026/12/31

VISAAPACFLT【華南卡】全站商品 滿 $5,000 折 $400

活動規定:點擊有信用卡合作的指定連結才能使用

HUWNAN2640001

Cee

Credit Card VeteranCredit card veteran. Lives on a NT$30K monthly salary but saves NT$20K a year through cashback — treats every purchase as an optimization problem. Studies cash back rates, points, FX multipliers, and multi-card stacking to figure out which card pays back the most.

You May Also Like

JR Pass 2026: Is It Still Worth It? 5 Summer Route ROI Recalcs

After the JR Pass jumped to ¥50,000, is it still worth buying for summer 2026? I lost ¥20,000 on the wrong pass last year. Here I recalc 5 typical summer routes (Tokyo–Kyoto–Osaka, Hokkaido, Kyushu + Sanyo, Fuji–Kyoto, 7-city wide) against single tickets vs regional passes, plus a 3-rule decision tree and JCB credit-card stacking.

First-Time Tokyo? 5 Traps That Catch Even Seasoned Travelers (2026 Entry Rules Update)

First-time Tokyo trip and stuck on Narita vs Haneda? Honest takes on JR Pass, the 2026 power-bank 100Wh rule, the new tax-free refund system, and the credit-card foreign-transaction fee that quietly eats your savings.

Best Overseas Card 2026: 6-Card Cashback PK, NT$3,186 Gap

I ran 6 overseas cards through the math after the 1.5% FX fee, then stacked Klook, KKday and Agoda bank codes. One NT$30,000 trip, NT$3,186 saved.